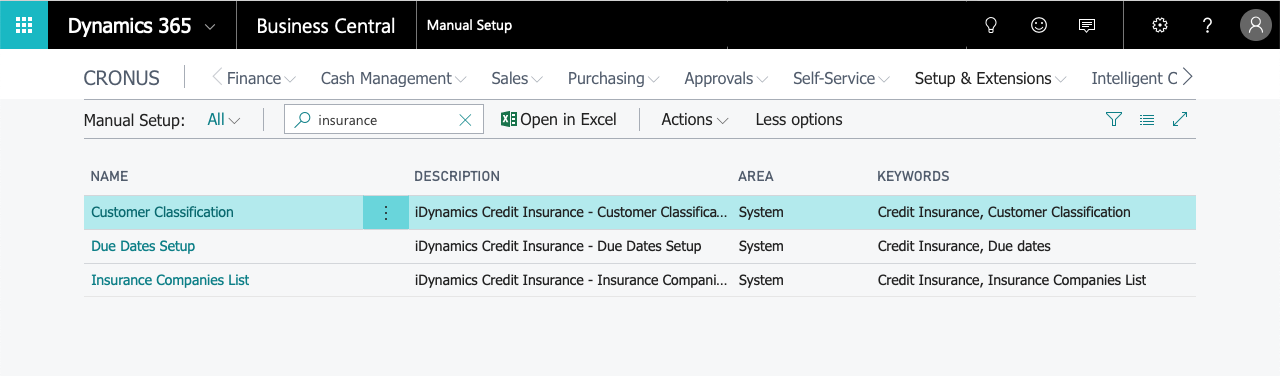

Usage instructions

You can access to due dates setup, to customers classification and insurance companies list from the manual setup page.

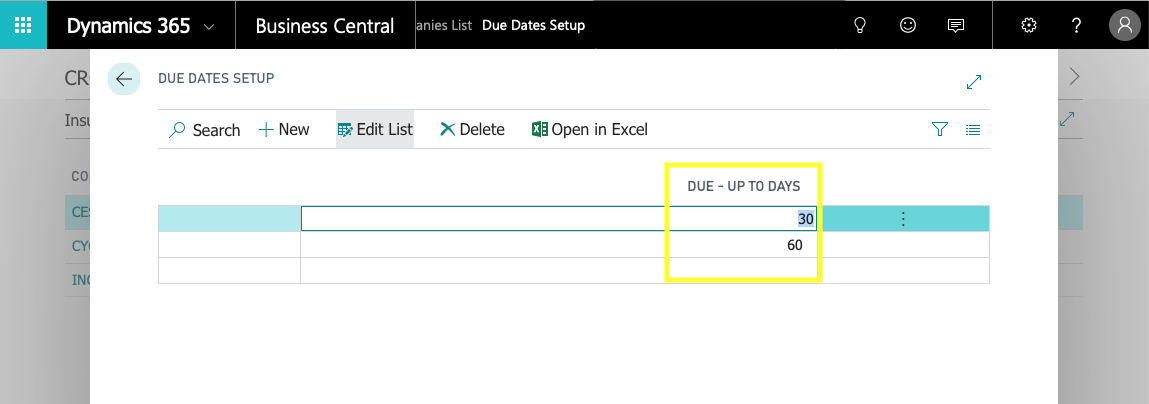

Due Dates setup

In this table you define the grouping intervals by Number of days from the date of sale to the due date.

Where the difference between the date of sale and the due date is higher than the last interval, they are grouped under the heading "More than [the last value in the table]".

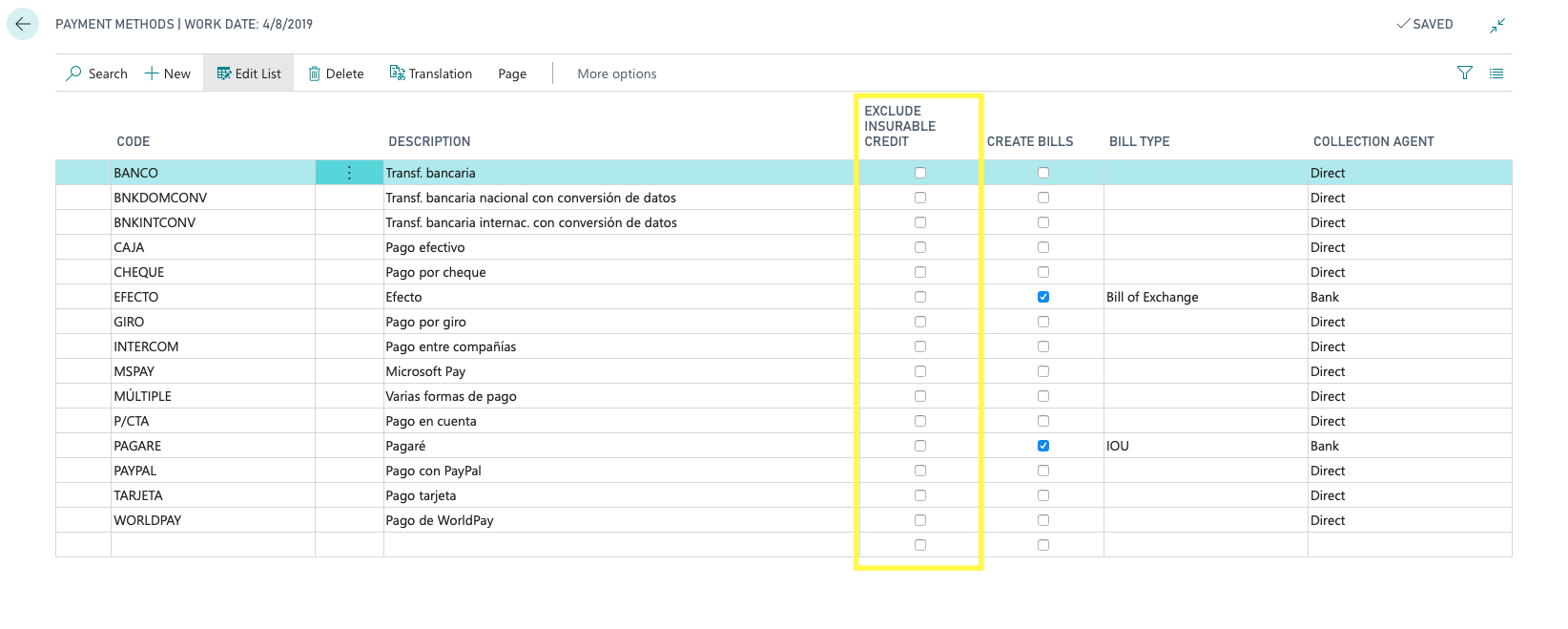

Payment Methods

From the "payment mehods" window, we can indicate whether this payment method is to be excluded from insurable credit:

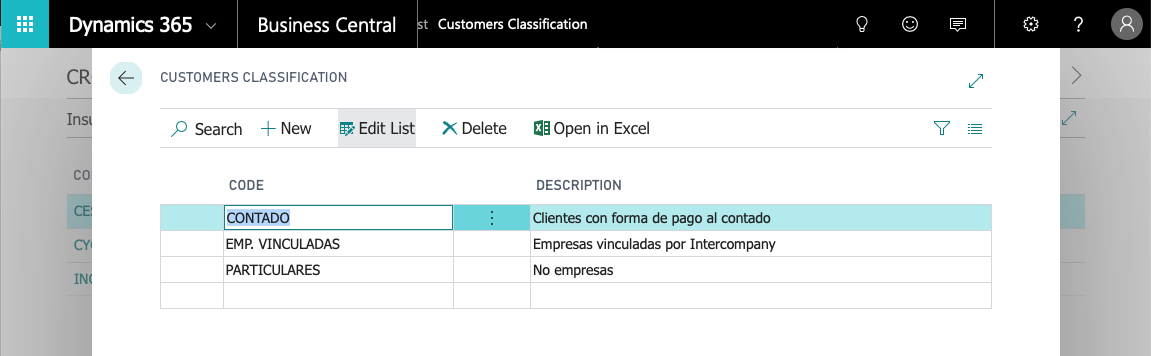

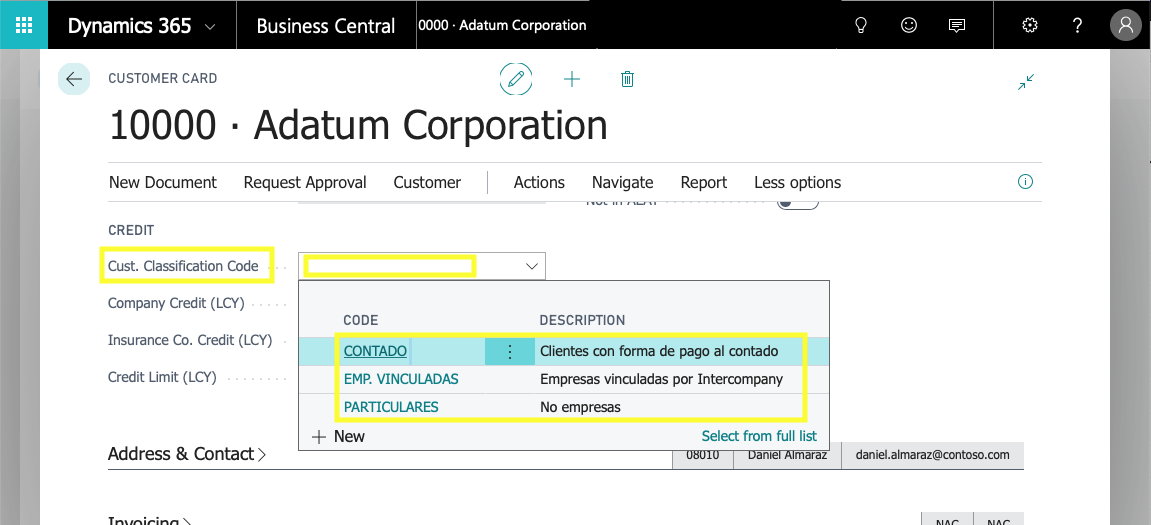

Customers Classification

These are the grouping codes for customers without assigning credit insurance.

You assign the clasification code in the customer page.

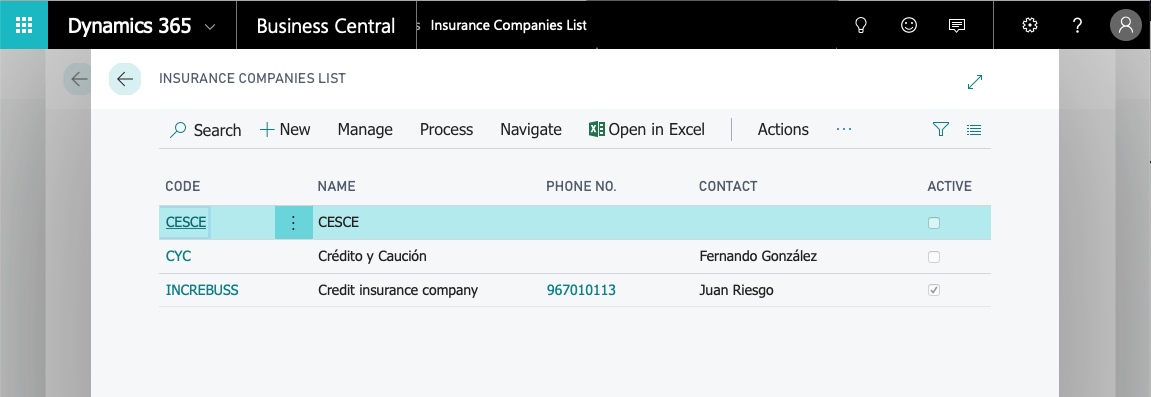

Insurance Companies list

From the Company information tab, the action Lists insurance companies leads us to their maintenance.

The first time we access this page we will find the list empty. From this page we will maintain the table Insurance companies and will facilitate access to the management of the Insurable credit policies and the Allocation of credit to customers.

The actions that we will be able to execute from this page will be:

- Manage the files of Insurance companies

- New

- Edit

- Delete

- Process Insurnce Companies.

- Activate insurance company

- Deactivate insurance company

- Navigate

- Insurance credit policies. Is the access to the credit policies dependent on the insurance company.

Insurance company

From the list of Insurance companies we will access the files of Insurance companies.

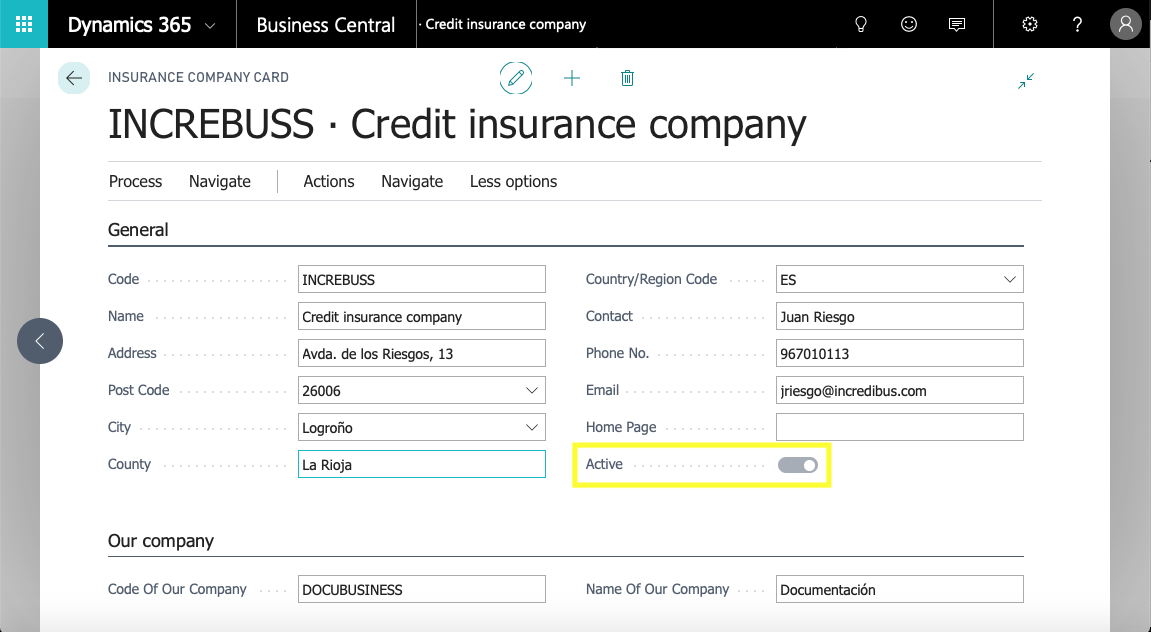

Once we execute the "New" action, the system shows us the "Insurance Company" page where we will fill in the information about the company.

Active insurance company

The card is automatically activated as it is the only insurance company in the table.

For later registrations of new insurance companies, the activation will be manual.

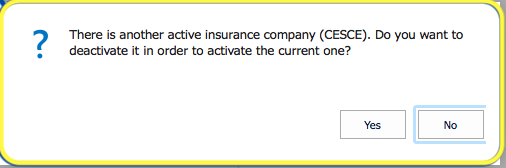

When an "active" Insuracne company file exists and we want to activate a new company, the systema will warn us about the existence of the previous one and will propose us its deactivation.

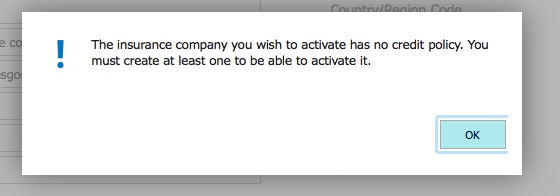

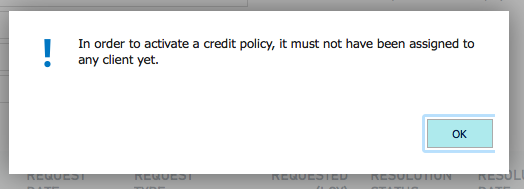

If the new insurance company has no policy defined, the system warn us of the circumstance and does not let us continue.

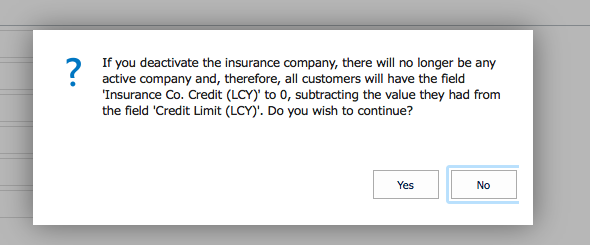

Disable insurance company

The function allows us to stop using the policy that is active and dependent on the insurance company. If the policy was assigned to a client, the system indicates this circumstance and the result after the desctivation.

Insurable credit policies

An insurance company must have credit policies assigned to it in order to be activated. For the same insurance company, you can create as many credit policy cards as you want, but only one of them wll be active.

When we activate an insurance company and it only has one policy assigned to it, the policy is automatically activated.

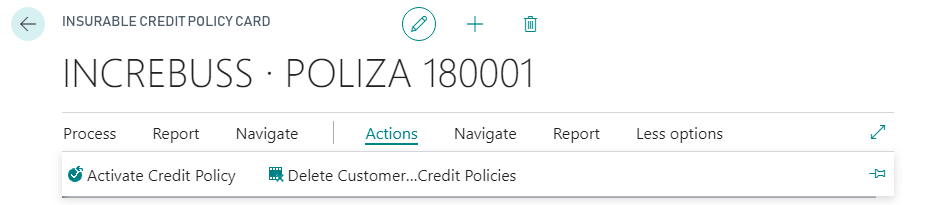

List of insurable credit policies

- Manage

- New

- Edit

- Delete

- Process

- Activate

- Delete customer credit policies

- Report

- Print policy

- Navigate

- Customer credit policies

Credit policy statement

The credit policy form consists of two parts:

- A part referring to the policy itself and its characteristics.

- Another part refers to the assignations of insurable credit assigned to customers.

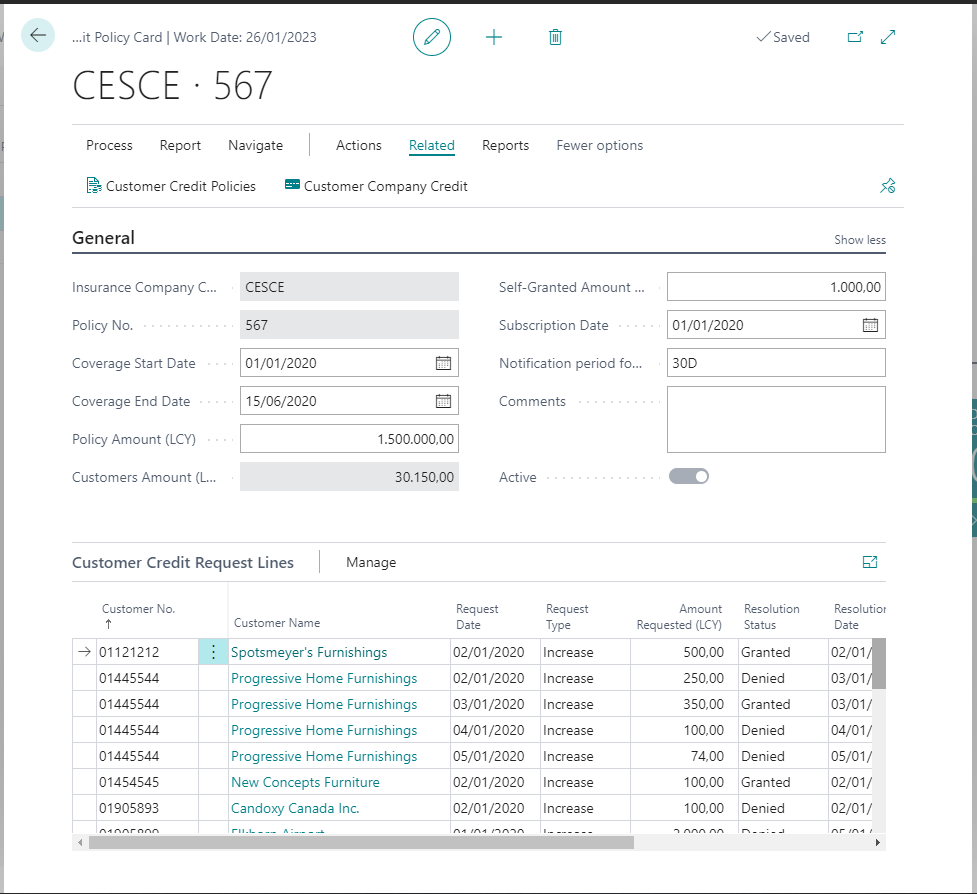

The identifier of a credit policy is the insurance company code and the policy number. In order for a credit policy to be active, the required fields are:

- Policy no

- Coverage start date

- Date of end of coverage

Other fields are:

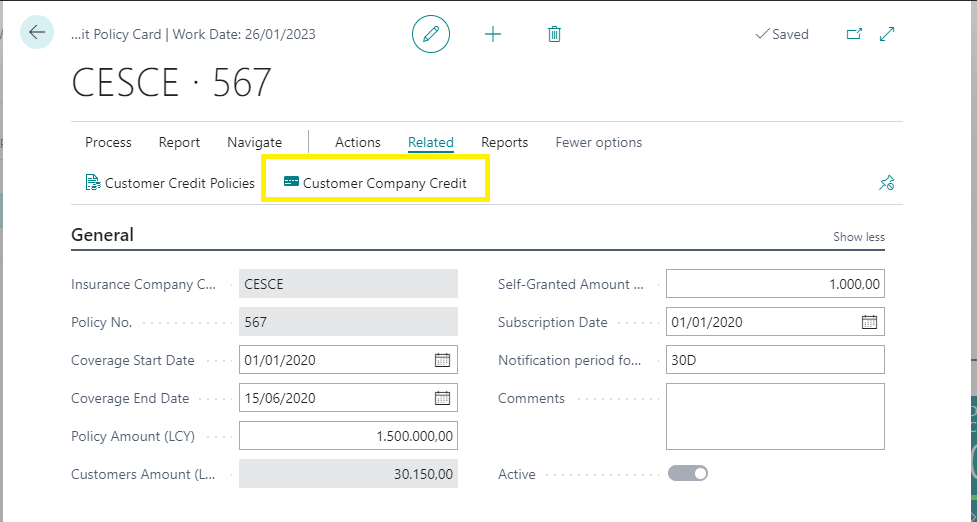

- Policy amount (DL). This corresponds to the amount, in Local Currency, contracted with the insurance company.

- Customer amount (DL). Corresponds to the amount insured in clients.

- Self-granted amount (DL). Credit assigned to clients without express request to the insurance company.

- Date of subscription. Date on which the policy is taken out. It does not involve any type of validation with respect to the rest of the information.

- Deadline for notification. It informs about the period of time available to us to inform the company of the non-payment of any of the customers with credit coverage. This is a date formula field.

- Comments. Free text field.

- Active. Indicates the status of the policy. This field is controlled in an automated way, through action functions.

In the menu of the card we have the options of handling a credit policy.

Auto Credit granted

Description / Generalities:

- Self-granted credit allows to automatically assign credit to clients (insurable), without the need to make an express request to the insurance company for said client. The amount of the self-granted credit is established in the policy file.

- A new field "Self-granted amount" has been added to the policy file.

- Self-granted credit is reflected as a credit request and is identified by a new Boolean field (“self-granted”).

- Self-granted credit applications can be accessed both from the credit policy file and from the customer's own credit policy. By default, auto-granted policies are not shown because they are filtered, and there is an action that includes or hides them from the list.

- Self-granted credit applications do not add to the amount of the policy.

- Self-granted credit applications do add to the maximum credit field of the client's file (standard field).

- When a “normal” credit application (requested from the insurance company for a client) is approved or rejected (not when created), if you have a self-granted credit application, it is canceled by creating a self-granted credit application for the same amount that was granted but in the opposite sign. It could be the case that a client had self-granted credit and was left without insurable credit because the application was rejected and also the self-granted credit was canceled.

Creation of self-granted credit applications:

- Automatically: when the auto-granted amount of an active policy is modified.

- If the amount changes from 0 to an amount> 0. They are created for all customers who can have self-granted credit; that is, they do not have a customer classification code, or form or payment term that excludes the insurable credit and that does not have the “IC Partner Code” field filled in and that they do not already have normal requests.

- If the amount changes from an amount> 0 to 0. Self-granted credit applications are eliminated only if they do not have normal applications.

- If the amount changes between amounts other than zero.

- If the client does not have normal requests, the self-granted credit request is regenerated for the new amount. The self-granted credit line is always created with the policy coverage start date.

- If the client already has normal applications, the possible self-granted credit application is not modified because the self-granted credit will already be canceled by having generated the normal application.

- Manually: from the customer file from the action "Update auto-granted credit" which acts in the same way as the automatic creation mentioned in the previous point but only for the customer in question.

- Manually: from the customer list: Same action "Update auto-granted credit" for all selected customers.

- When modifying a customer's file, if any of the 3 fields involved (payment methods, payment terms and classification code) have changed, the user is notified to execute the self-granted credit creation action. (It is only shown if there is an active credit policy with a self-granted amount)

- When entering a client's file, it is verified if he meets the conditions to have self-granted credit and if there is any irregularity, it is notified to remind the user to execute the action "Update self-granted credit".

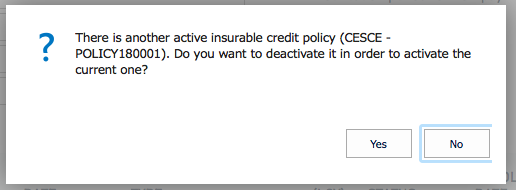

Activate credit policy

When this action is executed, the existence of an active credit policy is checked.

If there is an active credit policy, it is indicated by a message. The message tells us the number of the active policy and the insurance company to which it belongs.

Answering Yes, the function deactivate the indicated policy and will activate the policy of the card.

If the policy to be activated already has customer assignments, the function will indicate this with a new message.

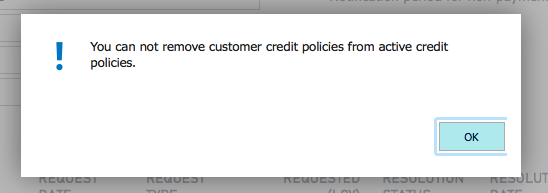

Delete customer credit assignments

To remove customer assignments from an insurable credit policy, it must be inactive.

If we try to remove the customer assignments and the source policy is not inactive, the function displays a warning message.

If the credit line is active, the function displays the list of assignments of the credit policy.

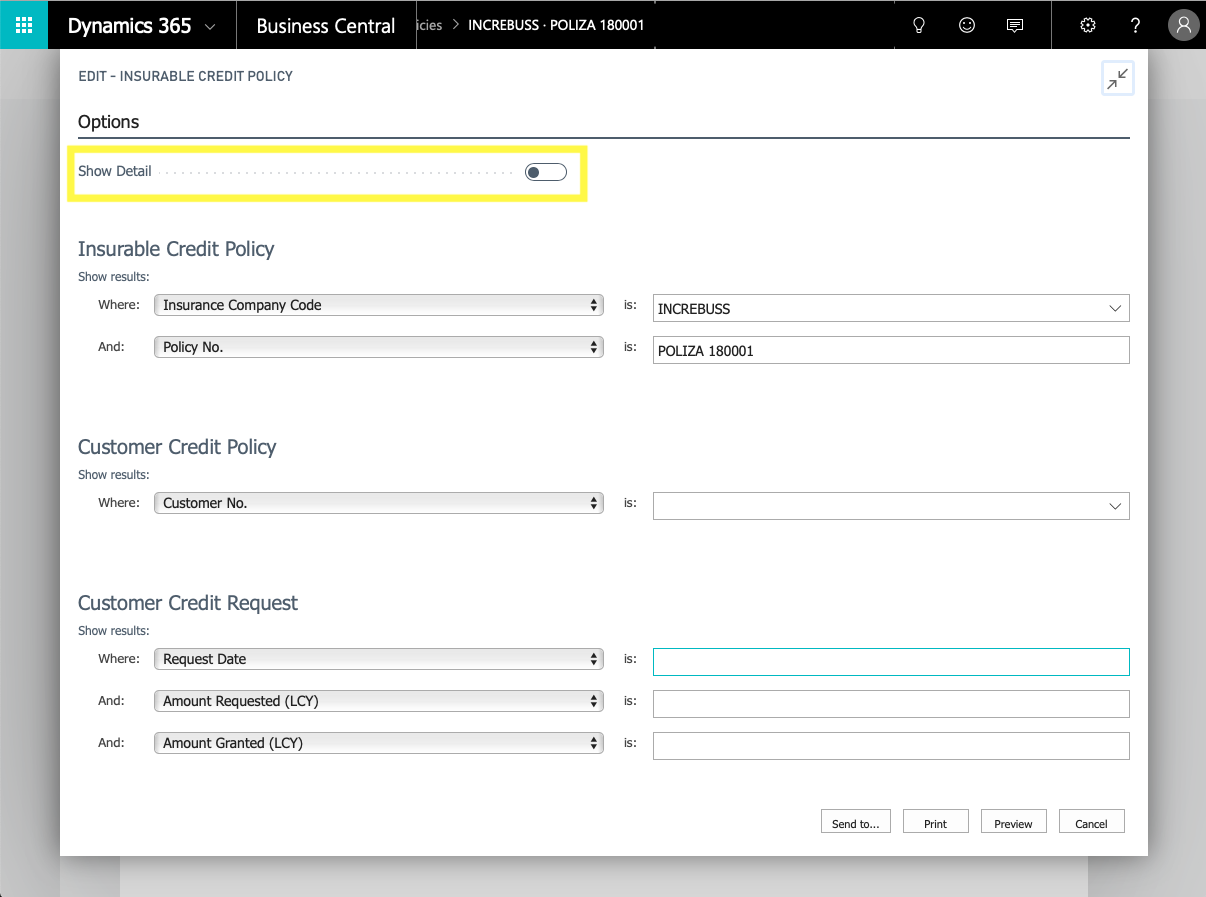

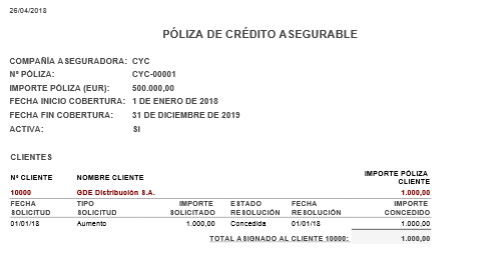

Print policy

Printing a credit policy presents some selection options.

In addition to Microsoft Dynamics 365 Business Central's own options, we can determine whether the report shows us details of customer assignments or not.

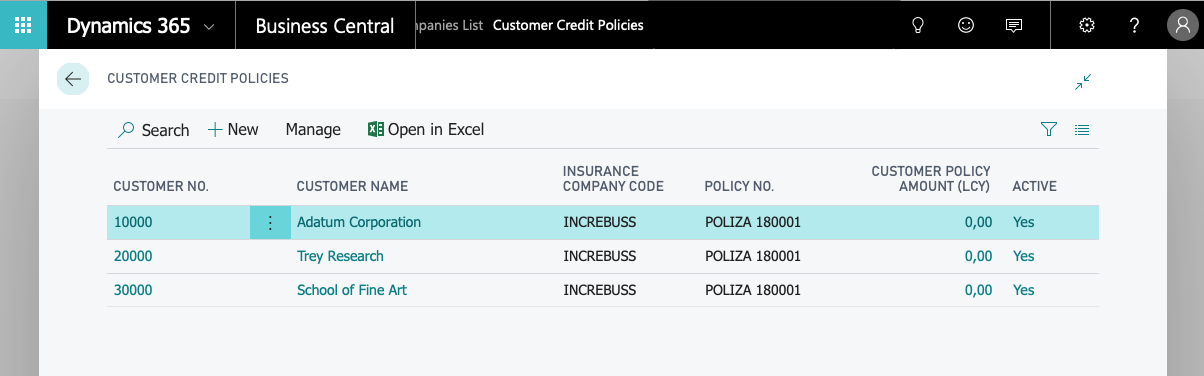

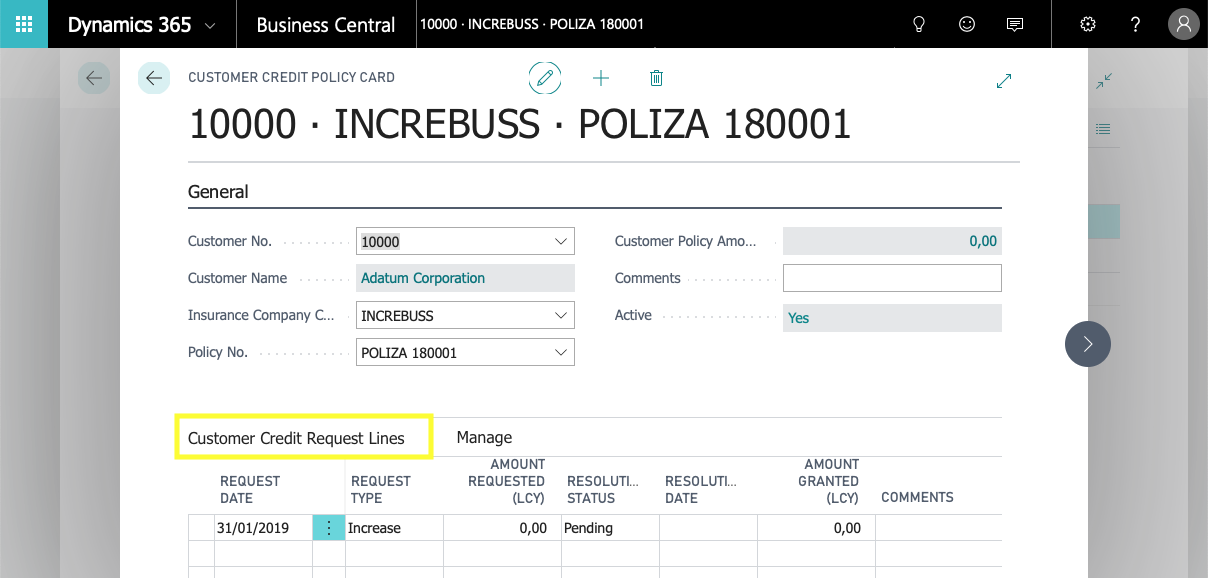

Customer credit policies

Shows the list of customers with assigned credit policy.

From the "Customer Credit Application Lines" subform we can manage the allocations of insurable credit for all our customers.

Customer credit application lines

The Insurable Credit Policy Form page contains a drop-down list showing the different actions taken with the insured customers. From this dropdown we can create the credit policy assignments to customers. Automatically, if the customer refered to in the application does not have a customer credit card assigned to him, he will be registered.

In the drop-down menu you will find the following fields:

Customer no.

- Must exist in the Customers table.

Customer nam.

- Recovers from the Customers table. It is non-editable.

Date of request for the action to be taken.

- Must be equal to or higher than the effective date of coverage and less than or equal to the effective date of coverage.

- There cannot be two applications for the same customer with the same application date.

Type of request. It only allows two possible "Increase or Decrease" values.

- Amount requested (DL). Coverage ampunt, in local currency, requested for the action indicated.

- If the action requested is "Increase", the amount will always be positive.

- If the action requested is "Decrease", the amount will always be negative.

- Status of the resolution.

- The difference possible values are:

- Pending

- Granted

- Denied

- The initial status is "Pending". Once changed to nay of the other values, it can no longer be modfied.

- The difference possible values are:

- Resolution date.

- It shall be indicated whenever the status of the decision is "Granted" or "Denied".

- If the status is "Pending", its assignments is not allowed.

- The resolution date cannot be earlier than the start coverage date of the credit policy, nor later than the end coverage date of the credit policy.

- Amount granted (DL).

- It will be assigned whenever the status of the application is charged to "Granted".

- It may not exceed the amount requested.

- Comments.

- Free text

Customer company credit

From the policy we can access the client company credit.

From the client company credit list we can manage the client company credit assignments.

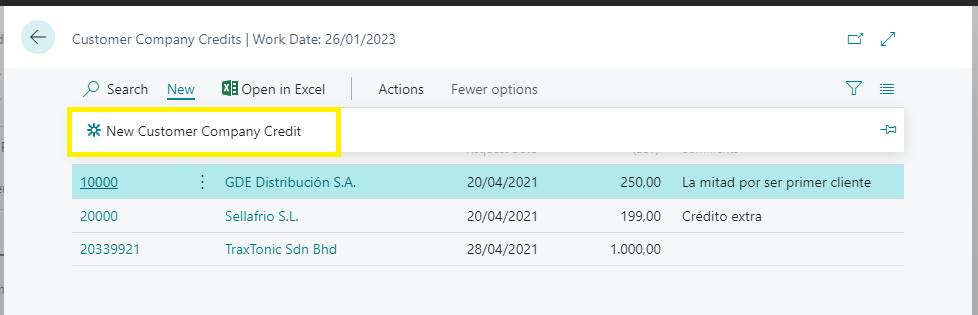

Company credit application

From the company credit list we can create new company credits.

Clicking on it will display a list of clients so that we can select the client to whom the company is going to grant credit.

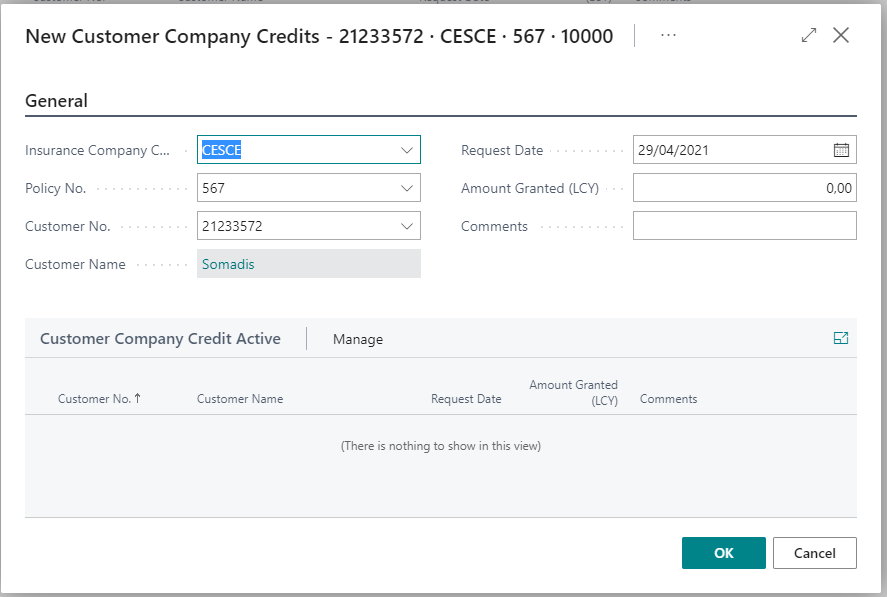

In the file we find the following fields:

Customer number.

- It must exist in the * Clients * table.

Client name.

- It is retrieved from the * Clients * table. It is not editable.

Date of request of the action to be carried out.

- It must be equal to or greater than the coverage start date and less than or equal to the coverage end date.

- There cannot be two requests for the same client with the same request date.

Amount granted (DL).

- It cannot be higher than the amount requested.

Comments.

- Free text

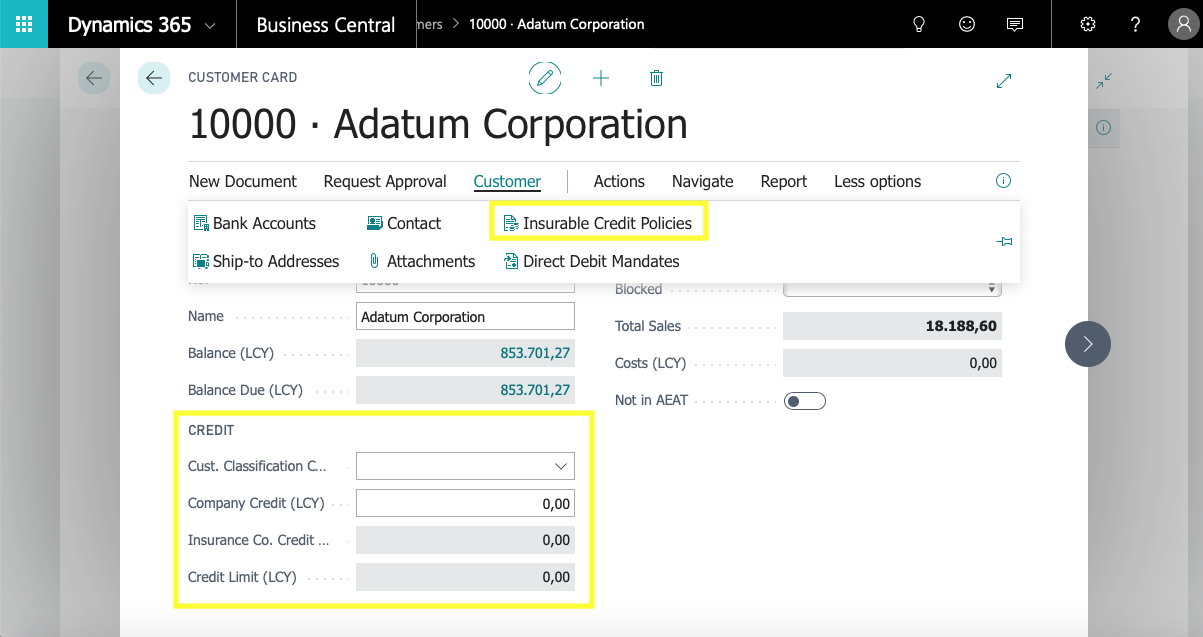

Customer

The customer tab contains all the information related to the customer. Regarding Insurable credit policies, we find the following fields and actions:

- Customer classification code

- From this window we will assign a classification code to the uninsured customer. This information is used in the Insured and Uninsured Sales Report.

- Company credit (DL)

- In this field, the uninsured credit granted by the company to the customer is assigned.

- This is an amount of cerdit in addition to the credit covered by the credit facility.

- The field is editable.

- Insurance credit (DL)

- This is a non-editable field. This is the sum of the amount granted (DL) for each customer credit application line.

Together with the company cerdit (DL), it constitutes the maximum credit granted to the customer.

- Maximum credit (DL)

- Field not editable.

Specifies the maximum amount by which the customer is allowed to exceed payment balances before appropriate warnings are issued. Consists of the insured and uninsured cerdit granted to the customer.

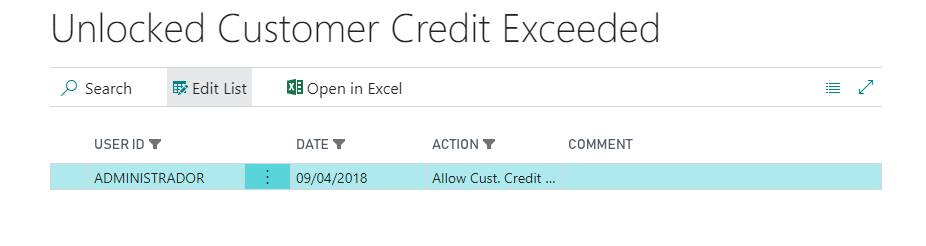

Maximum customer credit control

The control of whether a customer exceeds the credit limit granted is a standard function. The insurable credit function adds a lock action to the standard warning.

In the header of the sales order and the sales invoice, a field has been added "Allow overdue customer credit". The default value of the field is "False". For a user to be able to unblock the sales order, he must have *Read and Modify" permissions on the table "Unblock Customer Credit Overcome"(7142126).

Each time you block or unblock an order or sales invoice, a record is saved in this table "Customer credit unblocking exceeded".

The information stored in the table is:

The information stored in the table is:

- Action

- Action taken:

- Allow customer credit exceeded

- Do not allow customer credit exceeded

- Action taken:

- Date

- Date of implementation of the action

- User Id

- Document type

- Order

- Invoice

- No.

- Document number

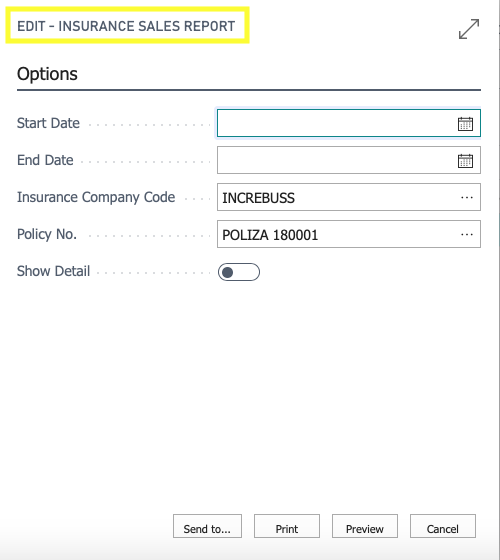

Sales Report for the Insurance Company

The report shows the insured and uninsured sales, within the specified period.

Groups the movements by days to maturity according to the values included in the table Setting due dates.

Displays all customer transactions whose Document Type is White, Bill of Exchange, Invoice and Credit Memo. Muestra todos los movimientos de cliente cuyo Tipo de documento sea Blanco, Efecto, Factura y Abono.

Note that the process of recording an invoice that generates bills of exchange creates three types of customer transaction record: the record of type "Invoice", the record of type "blank" for the settlement of the invoice and the record of type "Bill os exchange" for the conversion of the invoice in effect.

When requesting the execution of the report, it is assumed that there is only one active policy and that the policy belongs to the only active insurance company.

The user can determine:

- The start date: Date from which the customer movement records will be processed.

- The end date: Date up to which the customer movement records will be included in the process.

- See detail: Select or deselect. Indicates whether the report should show the details of the movements or not.

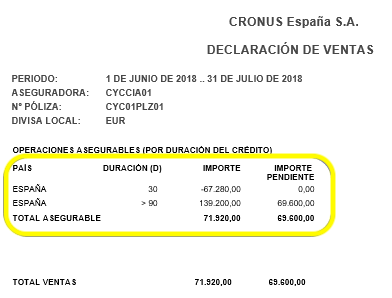

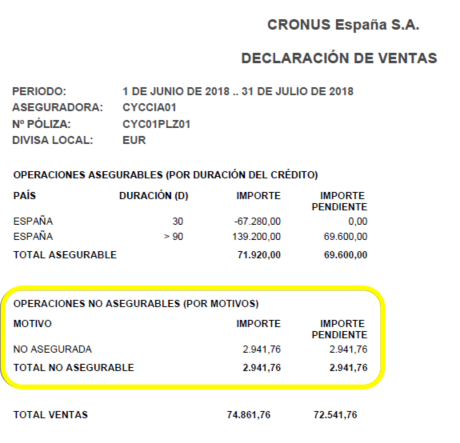

If we leave the "View detail" field unchecked, the result of the report will look like this:

If there were uninsurable sales the look would be:

For each of the countries to which the sale was made, a line is shown according to the period in which the days until the expiration of each sale are included. Displays the total of the amounts of the customer movements included in the report and the amount of such a sale that remains to be settled (risk).

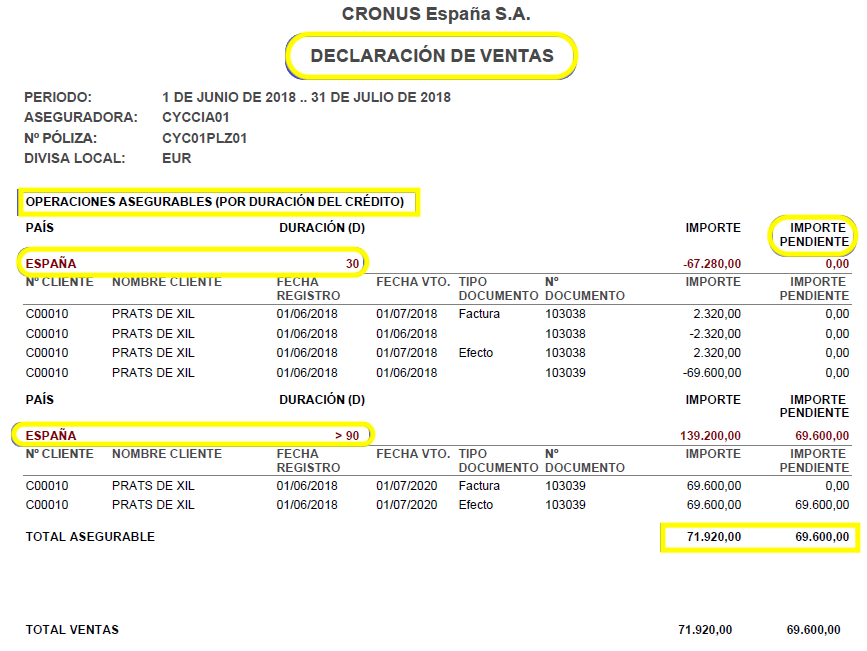

If we mark the "View Detail" field, the result of the report will be similar to that of the following image:

The difference with the previous report lies in the detailed information of the transactions that make up the amounts for each of the periods. For each of the customer movements, the following information is displayed:

- Customer number

- Customer's name

- Date of registration of the document

- Expiration date of the document

- Type of document

- Document number

- Amount of the sale

- Amount to be recovered

In both reports, both for the sales amount and for the amount to be collected, the following totals are shown:

- Total insurable

- Total uninsurable

- Total sales