Financial KPIs

This financial dashboard features key financial ratios essential for analyzing the business's performance. In addition to reviewing financial statements, it offers access to specific KPIs that fluctuate over time, enabling a quick assessment of whether the displayed values are within the target range.

The specific ratios depend on the financial statement being analyzed. Below are their definitions and the corresponding calculations.

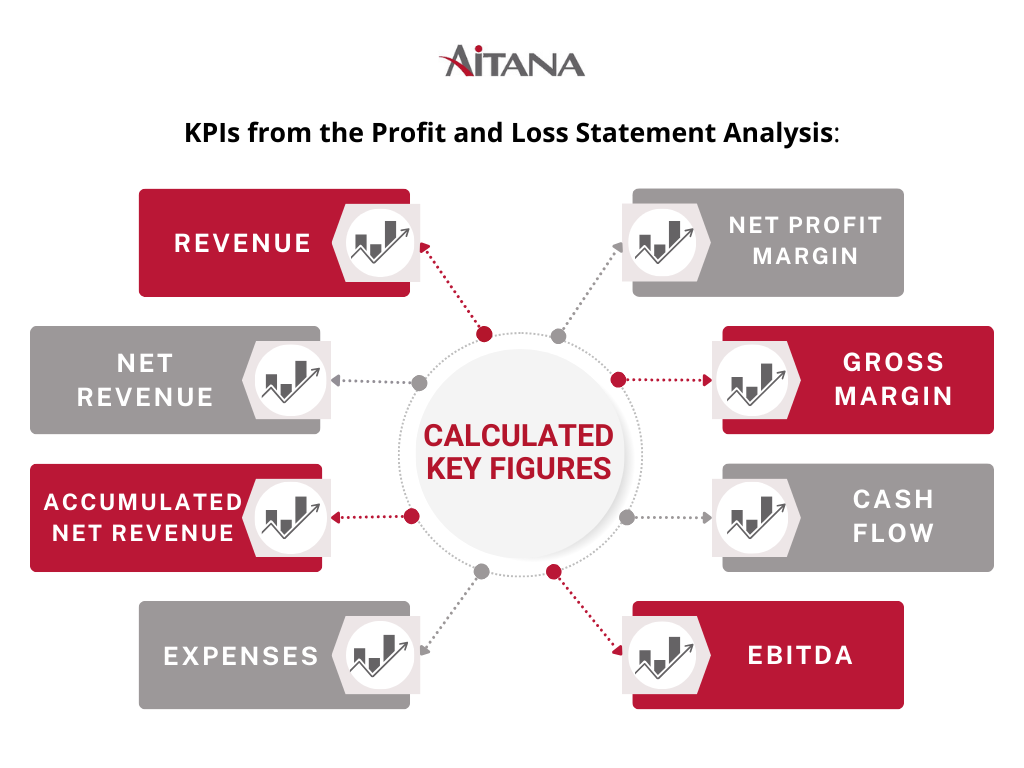

KPIs from the Profit and Loss Statement Analysis

Revenue

Calculated from the total revenue sum, which includes amounts in accounts of group 7, such as net turnover, work performed by the company for its assets, other operating income, and financial income, among others.

Net Revenue

Derived from the sum of revenues belonging to the net turnover amount.

Accumulated Net Revenue

The sum of net turnover revenue accumulated to date.

Expenses

Obtained from the total expenses sum, including amounts in accounts of group 6, such as supplies, personnel expenses, operating expenses, impairment, financial expenses, etc.

EBITDA

A financial indicator (Earnings Before Interest Taxes Depreciation and Amortization) that shows the surplus of operating revenue over the expenses related to these revenues.

To calculate it, start with the operating result (EBIT) and subtract the sum of amounts in accounts of groups 8 and 11 related to the depreciation of fixed assets and the impairment and disposal results of fixed assets.

Cash Flow

This concept refers to the movement of incoming and outgoing money in a company, showing liquidity for a specific period. It is calculated by subtracting from the total profit and loss account the sum of accounts in groups 8 and 11 related to depreciation and the impairment and disposal results of fixed assets.

Gross Margin

Defined as the difference between the income a company earns from selling its products or services and the direct cost of producing those products or services.

In this case, it is obtained by dividing the Operating Result (EBIT) by the net turnover amount, showing the percentage of each monetary unit of revenue earned as operating profit.

Net Profit Margin

This indicator measures the percentage of a company's total revenue that becomes net profit, reflecting the company's ability to generate profit after deducting all costs and expenses, including taxes and interest.

It is obtained by dividing the total amount of the Profit and Loss Statement by the total revenue (group 7 accounts).

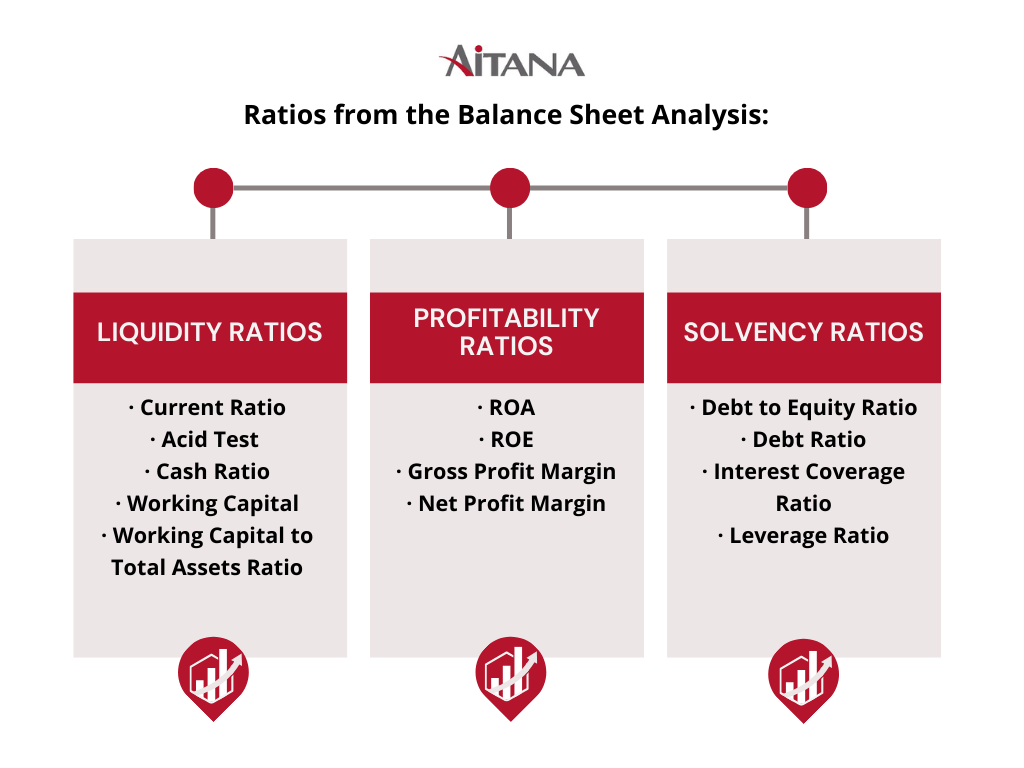

Ratios from the Balance Sheet Analysis

Liquidity Ratios

Current Ratio

This ratio measures a business's ability to meet its short-term obligations. It is derived from dividing current assets by current liabilities, with the resulting value indicating how many monetary units are available in current assets for each monetary unit of current liabilities.

Quick Ratio or Acid Test

The acid test measures a company's ability to pay its short-term debts using its most liquid assets. Unlike the current ratio, the acid test excludes inventory from the calculation. It is obtained by dividing the difference between current assets and inventory by current liabilities, indicating how many monetary units a company has in liquid assets (excluding inventory) for each monetary unit of current liabilities.

Cash Ratio

The cash ratio shows a company's ability to meet its short-term liabilities using only cash and cash equivalents. It is calculated by dividing cash and cash equivalents by current liabilities, indicating the proportion of current liabilities that the company can cover with its cash.

Working Capital

Working capital is the difference between a company's current assets and current liabilities. It measures the company's ability to meet its short-term debts with its short-term assets, indicating the company's "cushion" to cover its short-term obligations.

Working Capital to Total Assets Ratio

This ratio is calculated by dividing working capital by total assets, indicating the proportion of the company's total assets financed by its working capital.

Profitability Ratios

ROA - Return on Assets

An indicator of the profits generated by the company's assets.

It is calculated by dividing net income by the sum of current and non-current assets, indicating the return proportion generated on the business's total assets.

ROE - Return on Equity

An indicator showing how much economic profit is generated from the company's own resources and investments.

It is derived by dividing net income by equity, indicating the return proportion generated on shareholders' equity.

Gross Profit Margin

The result of dividing the difference between net sales and costs by net sales, indicating the gross profit proportion obtained by the company after covering the cost of goods sold.

Net Profit Margin

Derived by dividing net profit by sales, indicating the net profit proportion obtained by the company after covering all costs and expenses for each unit of sales.

Solvency Ratios

Debt to Equity Ratio

Calculated by dividing the sum of current and non-current liabilities by equity, indicating how many monetary units of debt the company has for each unit of shareholders' equity.

Debt Ratio

Indicates the percentage of assets financed by debt, derived by dividing current and non-current liabilities by current and non-current assets.

Interest Coverage Ratio

Calculated by dividing EBIT by interest expenses, indicating how much the companies earn beyond what is necessary to cover their interest expenses.

Leverage Ratio

A key metric that evaluates the extent to which a company uses debt as part of its financing.

In simple terms, this ratio indicates how much of the company's capital is financed by debt compared to its own capital or equity.

It is derived by dividing total liabilities (current and non-current) by equity, indicating the percentage of assets financed by debt.